You can adjust your income and expenses to more accurately reflect your financial situation. The point is to make your accounting ledger as accurate as possible without doing any illegal tampering with the numbers. You have your initial trial balance which is the balance after your journal entries are entered. Then after your adjusting entries, you’ll have your adjusted trial balance.

Part 2: Your Current Nest Egg

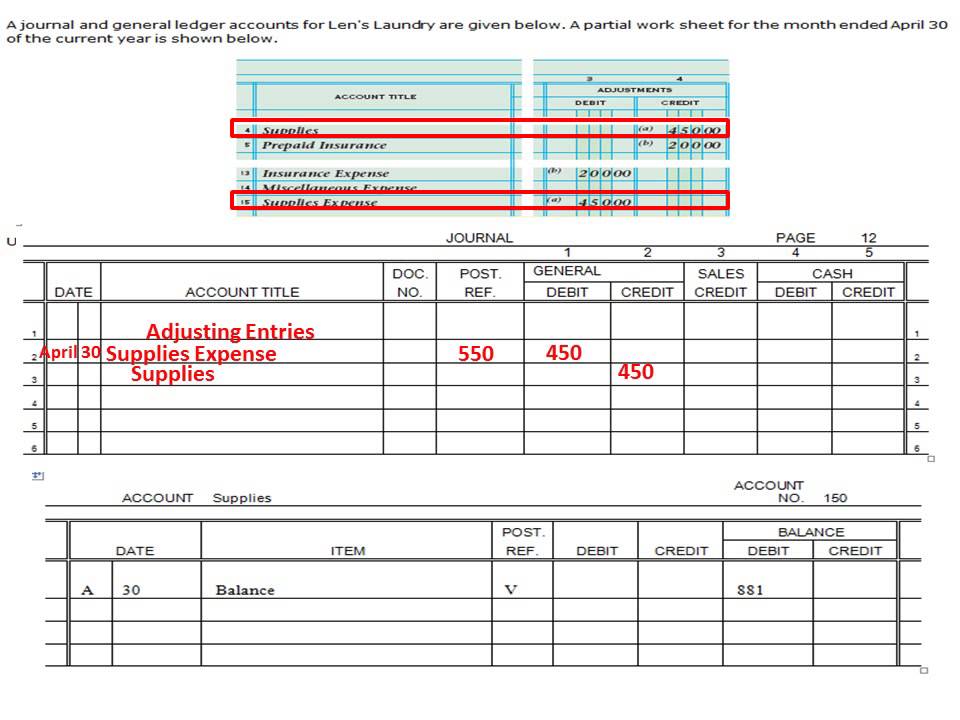

The preparation of adjusting entries is the fifth step of the accounting cycle that starts after the preparation of the unadjusted trial balance. A current asset representing the cost of supplies on hand at a point in time. The account is usually listed on the balance sheet after the Inventory account. And through bank account integration, when the client pays their receivables, the software automatically creates the necessary adjusting entry to update previously recorded accounts.

Accounting Adjustments

This is extremely helpful in keeping track of your receivables and payables, as well as identifying the exact profit and loss of the business at the end of the fiscal year. When you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 12 different Certificates of Achievement. First, during February, when you produce the bags and invoice the client, you record the anticipated income. However, in practice, the Trial Balance does not provide true and complete financial information because some transactions must be adjusted to arrive at the true profit. The main objective of maintaining the accounts of a business is to ascertain the net results after a certain period, usually at the end of a trading period.

- Accruals are revenues and expenses that have not been received or paid, respectively, and have not yet been recorded through a standard accounting transaction.

- Bench simplifies your small business accounting by combining intuitive software that automates the busywork with real, professional human support.

- Similarly, if a business incurs an expense in one period but pays for it in the next, an accrual entry is necessary to reflect the expense in the correct period.

- We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources.

- This misalignment can affect both the income statement and the balance sheet, leading to a skewed representation of the company’s financial health.

How confident are you in your long term financial plan?

Want to learn more about recording transactions as debit and credit entries for your small business accounting? When your business makes an expense that will benefit more than one accounting period, such as paying insurance in advance for the year, this expense is recognized as a prepaid expense. If you create financial statements without trial balance explained: your complete guide taking adjusting entries into consideration, the financial health of your business will be completely distorted. Net income and the owner’s equity will be overstated, while expenses and liabilities understated. Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance.

Deferred revenue is revenue that has been received but not yet earned. To record deferred revenue, an adjusting entry is made to decrease the liability account and increase the corresponding revenue account. It is important to note that adjustment entries are not recorded in real-time and are typically made at the end of an accounting period.

For instance, without adjusting entries, revenues might be overstated or understated, leading to an inaccurate representation of the company’s earnings. Similarly, expenses that are not properly matched with the corresponding revenues can distort the net income figure, misleading investors and other stakeholders. Recording transactions in your accounting software isn’t always enough to keep your records accurate. If you use accrual accounting, your accountant must also enter adjusting journal entries to keep your books in compliance. By recording these entries before you generate financial reports, you’ll get a better understanding of your actual revenue, expenses, and financial position.

These can be either payments or expenses whereby the payment does not occur at the same time as delivery. Not all journal entries recorded at the end of an accounting period are adjusting entries. For example, an entry to record a purchase of equipment on the last day of an accounting period is not an adjusting entry. Expenses are deferred to a balance sheet asset account until the expenses are used up, expired, or matched with revenues.

A common example of a prepaid expense is a company buying and paying for office supplies. These entries are posted into the general ledger in the same way as any other accounting journal entry. The purpose of adjusting entries is to show when money changed hands and to convert real-time entries to entries that reflect your accrual accounting.

Then, in February, when the client pays, an adjusting entry needs to be made to record the receivable as cash. The life of a business is divided into accounting periods, which is the time frame (usually a fiscal year) for which a business chooses to prepare its financial statements. This account is a non-operating or “other” expense for the cost of borrowed money or other credit. Usually financial statements refer to the balance sheet, income statement, statement of cash flows, statement of retained earnings, and statement of stockholders’ equity. A lag in recording transactions can also lead to incorrect financial statements. This can happen when transactions are not recorded in a timely manner or when they are recorded incorrectly.